Deductions Subject To 2 Floor For Estate

To Know The Tax Benefits Provided To First Time Home Buyers Watch Out Image Below To Grab These Benefits Just Call Out 8852 Finance Loans Loan Investing

Final Rules On Fiduciary Fees Are Issued Accounting Programs Estate Tax Tax Deductions

Buffer A Smarter Way To Share On Social Media Backyard Views Garage Style Backyard

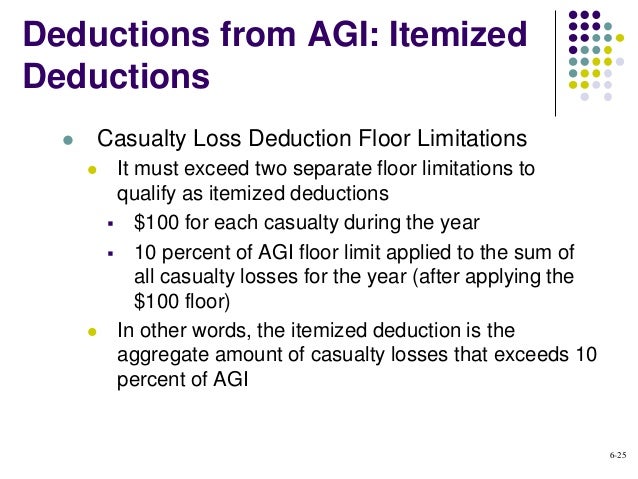

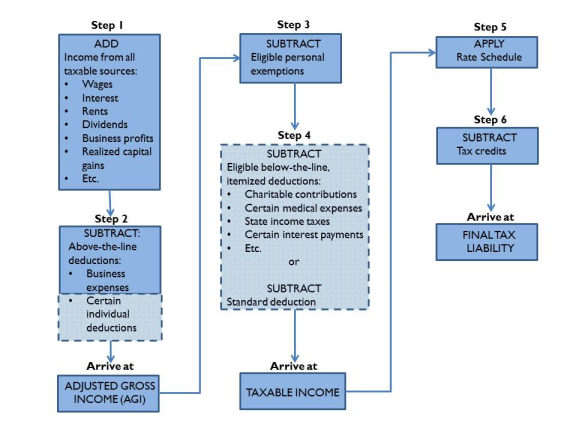

Acct321 Chapter 06

5 Br 4 Ba Home In Wellington Subdivision Carterton St Flower Mound Denton Isd Https Beautiful Travertine Floors Flower Mound Hand Scraped Hardwood Floors

Tax Deductions For Individuals A Summary Everycrsreport Com

Accordingly we conclude that the investment advisory fees incurred by the trust are subject to the 2 floor thus the 2 percent floor for estate or trust itemized deductions applies notwithstanding that the personal representative or trustee who may be held to the uniform prudent investors act may believe that the 2 percent floor does.

Deductions subject to 2 floor for estate.

Tax Time Tax Time Home Business Business Magazine

Price Drop Amenity Rich Gated Heritage Harbor In The Steinbrenner Martinez Mckittrick School District Built In Desk Home Office Space Great Rooms

Payroll Management Software Payroll Management Payroll Software

Checklist Of Documents Required For Filing Tax Return Of Salaried Person Download This Checklist From Https Taxdosti Com Filing Taxes Tax Return Informative

The 8 Most Important Questions To Ask Before Hiring Any Moving Company Redfin Real Time Realestate Diy Ctrealtor Plainvi Real Estate Hiring Movers Realty

Custom Testimonial Prop Home Buying Tips Real Estate Tips Real Estate Signs

House Warming Gift Artwork From A Photo In Pen Ink From Giveamasterpiece Com House Portraits Custom House Portrait Photo Art Gallery

5 Bedrooms Detached Duplex For Sales At Magodo Lagos Sale House Duplex For Sale House

709 S Walnut Street Floor Trim Marysville Hardwood Floors

Million Mansion That Is Still On The Market Photos And Premium High Res Pictures Stone Mansion Mansions Exterior

Living Room Kitchen Floor Transition Livingroomideas Floor Kitchen Living Livingroomideas Room Transition In 2020 Home Hanging Curtains Home Decor

If You Think Have To Choose Between Being Eco Friendly And A Good Budget Think Again With These Energy Saving Hacks You Real Estate Home Living Room Designs

Tax Deductions For Vacation Homes Depend On How Often You Use It

Great Ideas I Like The Subtleness Of These Suggestions It S Not Just About Putting A Giant Cow In 2020 Farm House Living Room Farmhouse Living Living Room Designs

Sometimes Something Might Appear Expensive But It Always Depends What You Get In Return Therefore Don T Think Real Estate Financial Modeling Excel

37 Marmion Rd Melrose Ma Maureen Fuccillo 617 510 7063 And Susan Felic Home Loft Bed Home Decor

50 Cent Battles In Bankruptcy Court To Save His Connecticut Mention Former Home Of Iron Mike Tyson Is Subject In 50 Cent Mike Tyson 50 Cent House Poplar Hill

Notice Of Late Rent Free Printable Documents Late Rent Notice Rental Property Management Rent

Tax Breaks For Capital Improvements On Your Home Houselogic

Free Offer To Purchase Real Estate Pro Buyer Form Wholesale Real Estate Real Estate Forms Real Estate Contract

To Much Open Space Under Those Stairs Here Are A Few Great Ideas On What To Do With Don T Let That Space Go To Waste Under Stairs Stairs House Styles

Month To Months Residential Rental Agreement Free Printable Pdf Format Form Rental Agreement Templates Lease Agreement Free Printable Room Rental Agreement

For Sale 679 000 This Beautiful Custom Farmhouse Is The Summerfield Plan To Be Built On Private 3 Acres With Spring Fe Home Types Of Houses Building A House

Duplexes Are For Sale At Northern Foreshore Estate Chevron Drive Lekki Sale House Duplex For Sale Estates

Source : pinterest.com